How to buy, sell, broker or invest in private mortgage notes for cash flow!

The partial note purchase provides an alternative to the full buyout of a real estate mortgage note. Discover just how partials work along with the primary benefits and structuring tips. We will be covering the ins-and-outs of partials, including:

A partial is the purchase of only a portion of the note’s remaining payments. If a note had 360 monthly payments remaining, a full purchase would be the purchase of all 360 payments while a partial purchase would be for something less than all 360 payments. It gives investors (and sellers) flexibility to achieve their goals with investing or selling notes.

When a seller allows a buyer to purchase property on installment, the terms of repayment are usually spelled out in a Promissory Note or Real Estate Contact. Sellers have the ability to sell and assign their rights to future payments.

Let’s take a look at how it all works.

A real estate note has a balance of $90,000 at 9.0% interest payable in monthly installments of $1,140.08 with 120 months (or ten years) of payments remaining. When the seller sells all 120 remaining payments of $1,140.48 to an investor it would be considered a full purchase.

If the investor only purchased the next 48 monthly payments of $1,140.48 each then it would be considered a straight partial purchase.

Once the investor received the next 4 years of payments, the note would be reassigned to the seller and the seller would collect the remaining 72 payments (120 total payments less investors partial purchase of 48 payments leaves 72 payments remaining to the seller).

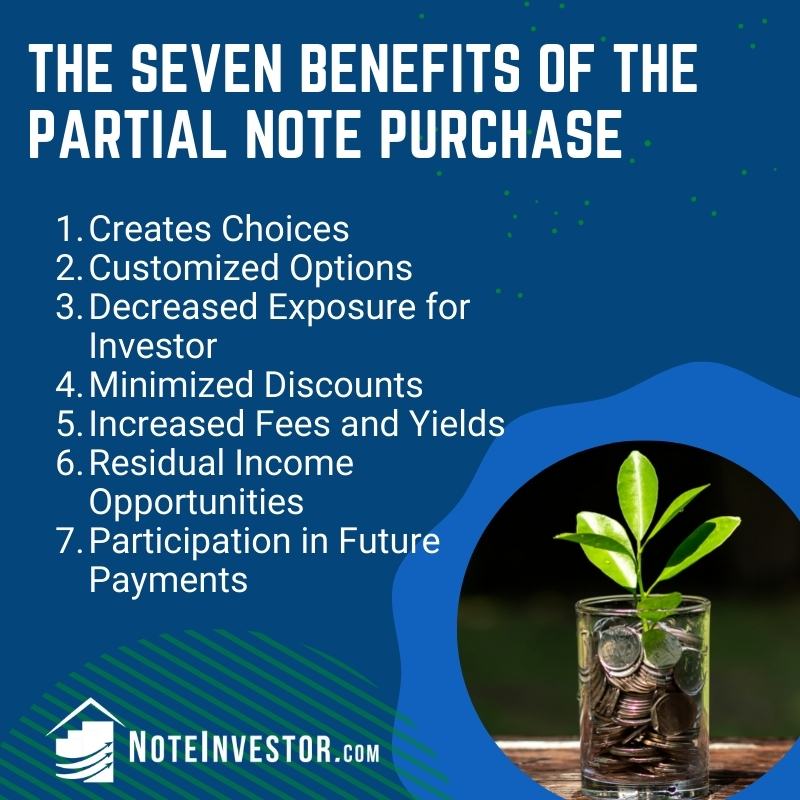

The partial purchase is one of the most powerful tools available to note buyers. Rather than providing one “take it or leave it” full purchase offer, the partial provides flexibility to design purchase options that meet the needs of the seller and the investor. Mastering the partial purchase will truly enhance effectiveness and profits by providing these primary benefits.

People enjoy feeling empowered to make a choice. The partial purchase helps empower note buyers. If the only option provided to the seller is for a full purchase, it sets up an all or nothing” scenario. The seller can either accept or decline. There are only two possible answers – yes or no.

Enter the partial note purchase offer.

Once a partial offer is added to the menu of choices, the seller now has two options they can consider. The partial instantly takes you from a 50% chance of receiving a positive response to a 66% chance of receiving an acceptance (that’s some math we can always get behind!). The seller now has more than one option to which they can answer, “Yes!” Presenting one full option and one or two partial options maximizes these improved odds for an acceptance.

As always, there is too much of a good thing. After three options are presented, anymore can become overwhelming. This can be a detriment, as a confused mind says “No!”

Even if the seller states they only want a full offer, provide at least one partial option. It will set you apart from the competition and create that environment of free will. If the seller questions receiving a partial in addition to the full offer they requested simply respond: “Our Company prides itself on providing choices. After reviewing your options, if you feel the full purchase is the best choice for you, we are happy to honor your preference.”

The impact of choice is amplified when the partial purchase is customized to meet the specific needs of the seller.

This takes knowing the seller’s motivation for seeking offers in the first place. If the seller has a $90,000 note but only needs $15,000 to pay for a child’s college tuition, they are more likely to prefer discounting just a portion of their note (say the next 36 monthly payments) to receive the desired cash, rather than discounting the whole thing.

Once the upfront cash needs of the seller are determined, it is fairly simple to calculate the number of payments that must be purchased to generate the cash investment at the investor’s yield.

The seller’s future needs can play a role in customizing the option in addition to their need for cash today. An elderly seller on a fixed income is unlikely to be excited about receiving the note back in 15 years to collect the remaining 15 years on a 30-year note. They are more likely to be interested in a partial structure that allows them cash now plus a split of the immediate payments to supplement their fixed income. The more customized the offer is to fit the seller’s needs, the greater likelihood they will choose to work with you.

Investors typically set maximum exposure rates for a transaction limiting the dollars available to invest in any given transaction. This Investment to Value (ITV) ratio will decrease as the perceived risk increases. When a transaction has a high Loan to Value (LTV) ratio, a lower ITV ratio can result in a high discount to the seller. A partial enables an investor to lower their exposure while still presenting an appealing offer to the seller.

The time value of money makes payments due sooner more valuable than those further out in the future. The partial minimizes the seller’s discount by allowing them to cash in the most valuable portion of their note – the more immediate payments. It also enables them to keep the face rate or interest rate of the note working for them on the portion they hold rather than sale.

Let’s take a look at that theory in action:

Scenario I – Full Offer

Consider a note for $100,000 at 10% interest payable in 360 monthly payments of $877.57. If the investor desires an 11% yield, the pay price will be $92,150.55.

Note Balance: $100,000.00

Cash at Closing – Full Offer: $92,150.55

Discount: $7,849.45

Scenario II – Partial Offer

If the seller elects to assign just half of the cash flow or the next 180 monthly payments the investor can pay $77,210.31 at an 11% yield. The initial cash at closing to the seller is reduced by $14,940.24 compared to the full offer but look at what the seller retains! When the note is assigned back to the seller in 15 years, the principal balance still owed by the payer will be approximately $81,665.21. The seller defers payment of the $14,940.24 in exchange for a balance of $81,665.21 in 15 years!

Note Balance: $100,000.00

Cash at Closing – 180 Partial Option: $77,210.31

Plus Remainder in 15 years: $81,665.21

Seller Receives Over Time: $158,875.52

If you have seen note buyers advertise “No Discount” or “We Pay Full Face Value”. they are usually just using some sort of partial purchase similar to this example. There is a sum of cash at closing for the partial purchase and then the balance is reassigned to the seller in the future, with the two combined amounts equaling or exceeding the principal balance at closing. This might also be structured as a two-stage buyout with cash at closing for the first partial stage, with another advance in the future for the seller’s remaining interest or the second stage.

While “No Discount” is an eye catching marketing phrase, it can also be misleading to the seller as they aren’t truly receiving 100% of the balance at closing. Rather it is received in stages over time. In order to avoid any confusion or claims of misrepresentation, we avoid using these marketing slogans and just present our options as partial purchases with money now and money later.

The discount is not the focal point on a partial purchase. This allows a consultant/broker to earn increased fees and an investor enhanced yields. When a full offer is made, the discount screams to be noticed but is subtler on a partial. Let’s look at that in action!

Scenario I – Full Offer

Assume the seller has a $90,000 note at 8% interest with 240 remaining payments of $752.80 each. The investor desires a 9% yield and offers $83,669.54. The consultant decides to earn a $3,000 fee resulting in an offer to the seller of $80,669.54. The almost $10,000 discount is usually the immediate focus by the seller.

Note Balance: $90,000.00

Investor’s Full Offer: $83,669.54

Less Consultant’s Fee: $3,000.00

Amount to Seller: $80,669.54

Investor Yield: 9%

Consultant Fee: $3,000

Scenario II – Partial Offer

If you take that same transaction and structure a partial purchase for the next 120 monthly payments of $752.80, the investor could offer to pay $58,177.30 at a 9.5% yield. The consultant desires a $6,000 fee resulting in an offer to the seller of $52,177.30 cash at closing. The seller also retains the right to the remaining 120 payments on the tail end with the note having an approximate remaining balance of $62,045.85 when the note is reassigned in 10 years. Provided the $52,177.30 meets the seller’s need for cash today, this is a win-win scenario for everyone. The investor increases their yield, the consultant increases their fee, and the seller gets to keep the note interest working for them which minimizes the impact of discount over time to the seller.

Note Balance: $90,000.00

Investor’s Partial Offer: $58,177.30

Less Consultant’s Fee: $6,000.00

Amount to Seller: $52,177.30

Plus Remainder in 10 years: $62,045.85

Seller Receives Over Time: $114,223.15

Investor Yield: 9.5%

Consultant Fee: $6,000

Frequently a note holder will only own one note. When a full purchase is made on their sole note, there are no opportunities for future residual income, unless that seller should once again sell a property and take back owner financing. A partial purchase is a way to turn this note holder into a repeat customer.

Once a partial is sold to an investor, an opportunity is created for repeat business with partials through the purchase of additional payments retained by the seller. In fact the partial agreement grants an option or first right of refusal to the investor should the seller elect to sell any additional payments in the future. This prospect enables consultants to earn additional fees and investors to realize further yields.

Once a partial purchase has been closed, be sure to add to your calendar for a return call in 12 months. This is a great time to touch base with the seller regarding the status of their remainder interest and whether they would like to sell all or part of their remaining payments.

The partial purchase creates a gateway for building long-term income by participating in the future cash flow of the note. This can be accomplished with little or no outlay of cash when utilizing an investor for the initial partial purchase. One of our favorite wealth-building techniques in the cash flow industry is the “Buy Full – Sell Short” strategy.

This strategy is based on your purchase of the full payment stream available on a note from the holder/seller with the resale of a shorter payment stream to an investor. This enables a cash flow professional to earn a commission on the initial sale of the partial payment stream to the investor AND keep a portion of the future payment stream as a personal wealth-building vehicle. The payments remaining after a partial investment pays off are also known as the “tail-end” or “back-end” of a note. Retaining these payments can often be accomplished with only an investment of time and without the investment of personal capital.

To illustrate the power of “Buying Full and Selling Short” using the partial purchase, take a look at the Church Note where we bought 306 payments of $1,096.96 per month, sold 186 to get whole, and kept 120 on the back-end.

There are so many ways to slice and dice a payment stream that the number of partial options available is only limited by your imagination! Let’s review the standard purchase structures utilized by investors.

The purchase of a note in its entirety.

The purchase of immediate installments with the seller retaining remaining future installments and/or the balloon payment.

The purchase of immediate installments up to and including a portion of the balloon payment with the seller retaining a portion of the balloon payment.

The purchase of a portion of each installment for a specified time and amount with the seller receiving the remainder of each installment.

The purchase of future installments allowing the seller to continue receiving immediate installments for a specified period of time.

The purchase of half the number of remaining payments for half the balance. This video on Calculating Note Investments Using the 50-50 Partial is a great example.

The purchase of the next twelve monthly payments for the price of ten payments.

The majority of investors will require the standard full assignment of the Mortgage or Deed of Trust to be recorded at closing. They will also require possession of the original note with a proper note endorsement. The Purchase and Sale Agreement outlines the amount of payments the investor is buying and the seller is retaining.

The Partial Purchase and Sale Agreement starts with the standard descriptive clauses, contingencies, and provisions for representations and warranties as found in the Full Purchase Agreement. Additional language is included to detail specific partial terms pertaining to the servicing, collection, termination, reassignment, and procedures for handling a prepayment or default.

When working with documentation it is important to review with legal counsel to avoid creating any type of security and to be certain all parties are protected in the event of early payoff or delinquency.

One of the challenges to the partial purchase is helping the seller understand how the payments will be divided.

Sellers wonder what is their portion of ownership and how will monies be disbursed in the event of an early payoff? They are fair questions.

While the partial purchase agreement provides the legal answers, the partial amortization schedule is a helpful tool providing a visual schedule for addressing these common questions. Many investors will attach the partial amortization schedule as an exhibit to the partial agreement resulting in the commonly used reference of Schedule B.

Ready to take the partial note purchase to the next level? Join us for the Perfecting Partials Master Class!